Chapter 2 The Recording Industry

The recording industry creates recordings for physical and digital sales, for public performance in radios, television, online and in public venues such as restaurants, hotels and shop. It also creates recordings to be synchronized with motion picture.

In the 21st century all over the world the live music is the main revenue stream for most artists, however, recordings have a far greater audience. In 2017 it is impossible to appear on live performances without a sound recording and at least a YouTube video.

The most comprehensive data source of the global recording industry is the annual report of IFPI, i.e. the Recording Industry in Numbers. The data are annually compiled by national IFPI chapters.

In Europe, we have three types of record markets.

In Western Europe, physical sales have stabilized and remain the main revenue source for recorded music. Cultural spending in these countries is sufficiently high to keep records in the stores, and large online retailers, such as amazon.de keep the product on offer. While sales is low compared to the 20th century, CDs and vinyl can keep their place in a relatively large music market.

In Northern Europe, and partly in the UK, culture spending is high and households have been enjoying very good internet connections and high-level digital services for a longer period. In these countries digital sales are the main revenue source, often for a longer period. For example, Sweden was an early pioneer of the model, and Swedish CMOs helped the creation of Spotify in the country.

The emerging markets are characterized by overall very low level of record sales, and musicians can almost solely rely on live music and grants for the livelihoods. Poland with her large internal market is a bit closer to Western Europe. The lack of a functional sound recording market is a trap for musicians, because in the absence of successful records it is more difficult to enter foreign markets and get noticed for film synchronization contracts.

In Central Europe, similarly to middle income Latin-American countries, performance revenues and synchronization revenues are relatively important, and collective management societies, music publishers part an important role in re-creating the domestic, national recorded repertoire.

2.1 Central European market characteristics

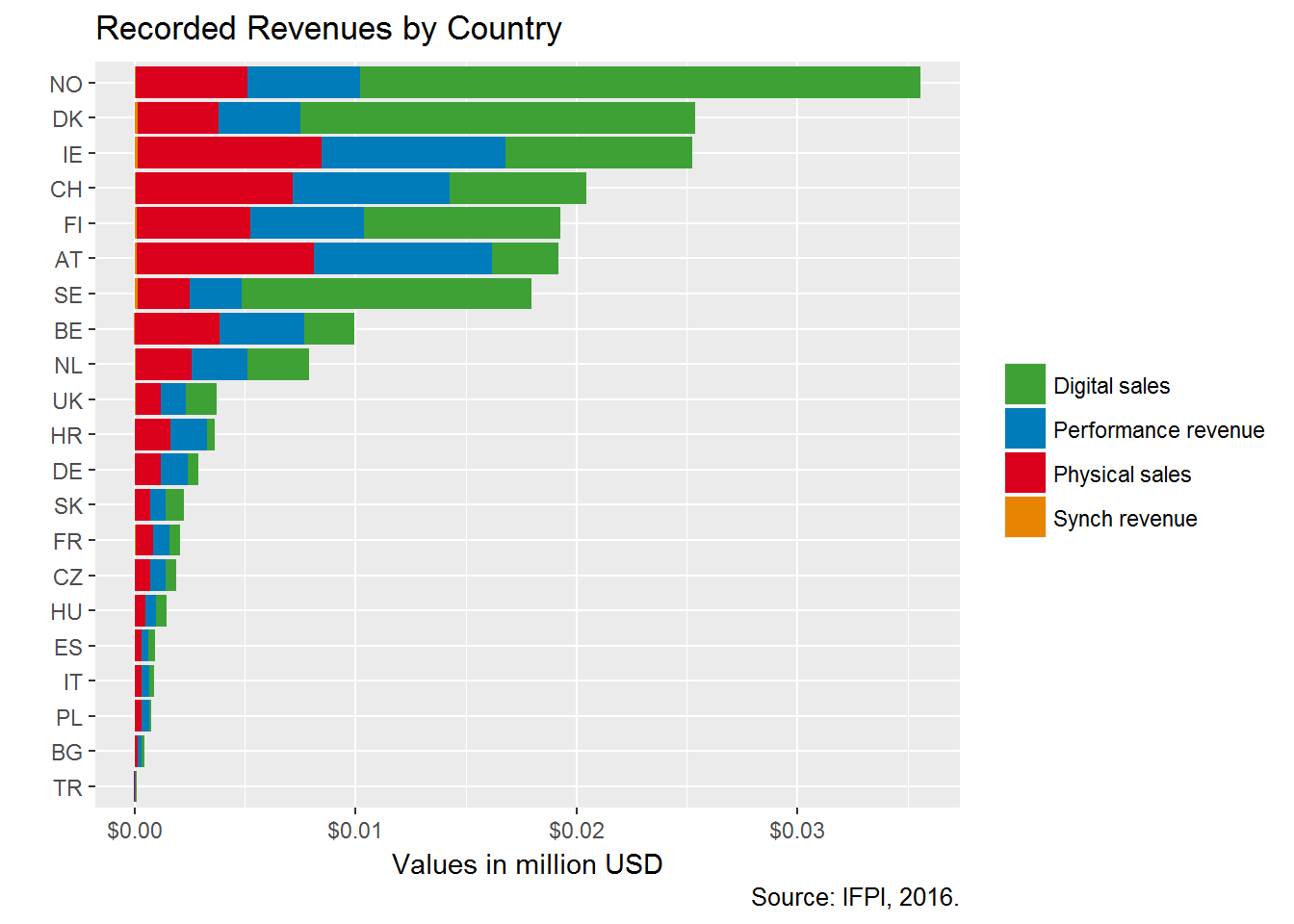

In the first figure we highlight the four main revenue types of the three major type of markets, projected as a per capita figure based on the country’s population.

(#fig:rin_revenues_abs)Recording Revenues by Country

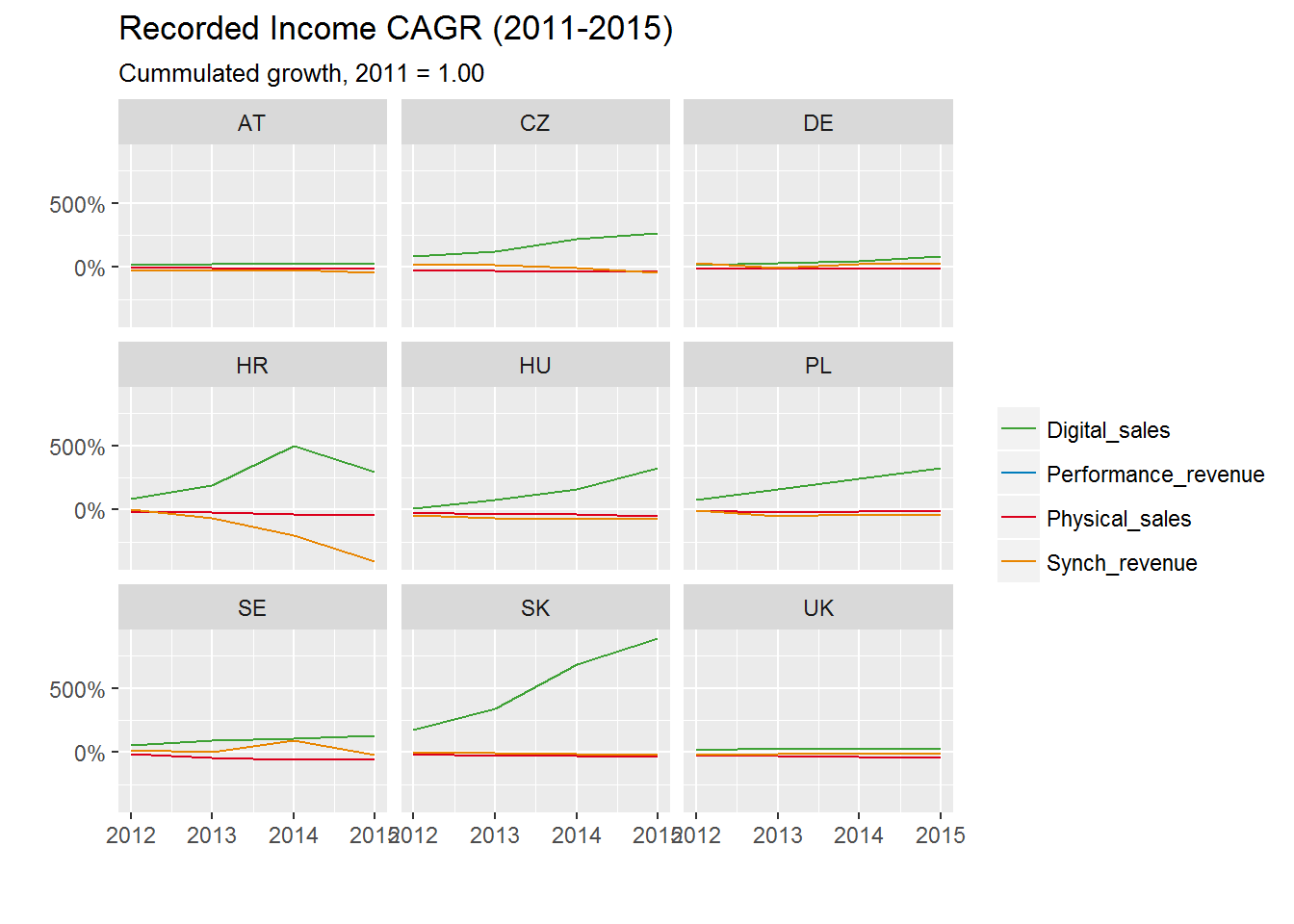

The main source of growth is digital sales; however, physical sales remains very important where the market has not collapsed. It larger countries, such as Germany or Poland the production and retailing infrastructure of physical records survived in a streamlined form. In smaller countries, there were not enough sales to keep the record shops and physical distribution alive, and records are almost exclusively sold on concerts. CDs and DVDs are still important temporary carriers of storage, and they are also ideal gifts or souvenirs. In the Czech Republic, Hungary or Slovakia revitalizing some sales point, together with the fast-growing physical segment vinyl could help stabilize recorded revenues.

In Continental Europe and Latin-America performance revenues also play a very important role. This is especially true in countries where households individually have a smaller cultural budget, but restaurants, clubs, radios and other B2B users pay licensing fees. Synchronization revenue is usually very ad hoc and small, but it certainly shows a high level of correlation with the local motion picture industry. Increasing synchronization is especially important for local musicians to reach a wider audience internationally, as music and television is crossing borders more easily than the now defunct record market.

2.1.1 Main income sources

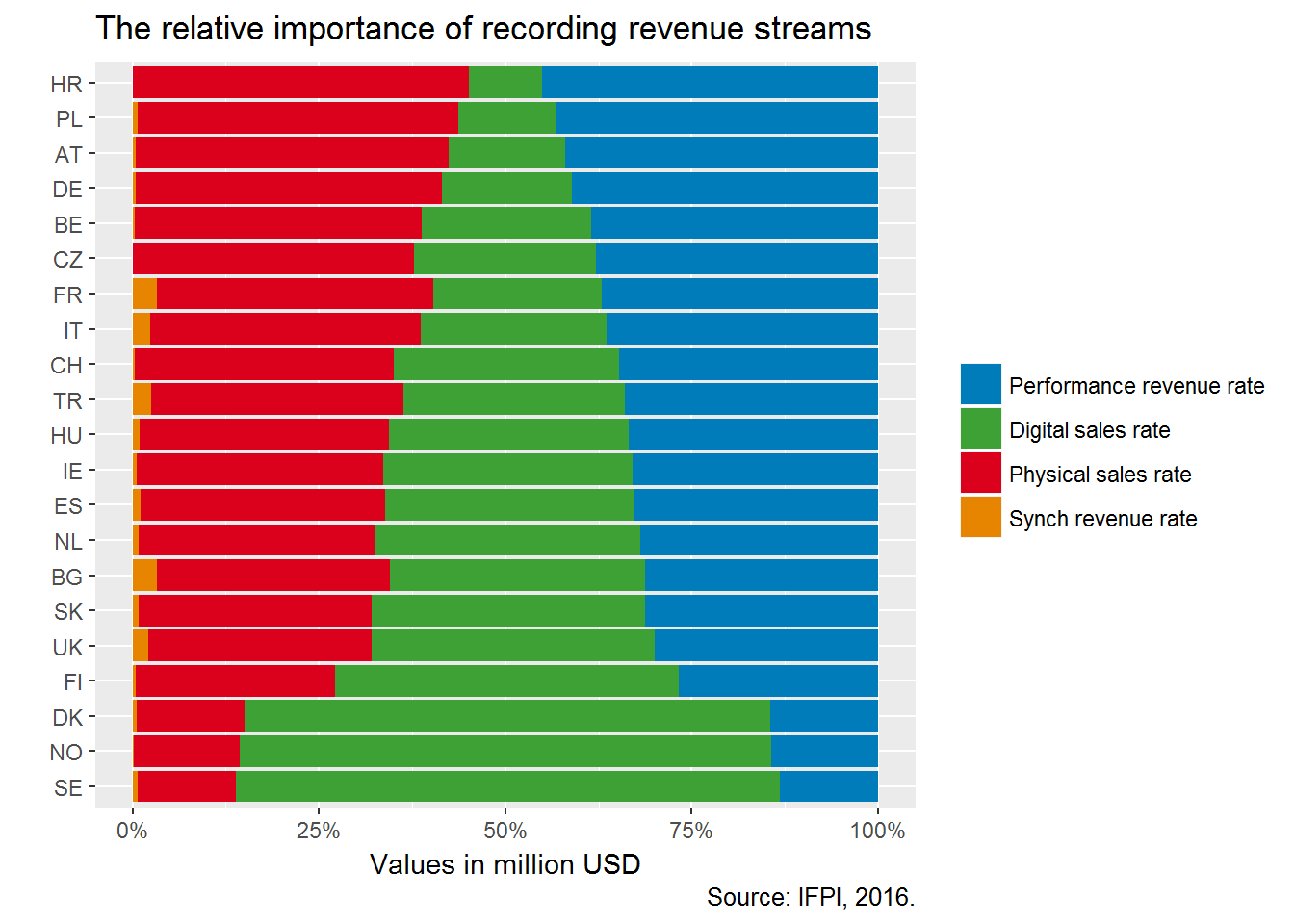

(#fig:rin_revenues_rel)The relative importance of recording revenue streams

The most typical Central European market is Croatia, where the traditional physical distribution is still more developed than digital sales. In this smaller market some of the important digital companies, such as iTunes are not present, and domestic companies could not develop the market it sufficient depth.

Germany and Poland are typical Continental, balanced markets with still high physical sales. Northern European counties that pioneered digital services, such as Sweden, which is the home of Spotify, almost exclusively rely on digital sales to households.

The region is an emerging region with a very high level of growth (from a tiny base) in the digital segment. The most important players are collective management societies that represent performance revenues and digital vendors. The key to success in the region requires a combination of good public performance and online presence.

2.1.2 Demand and home copying

People in Central and Eastern Europe do not have a much smaller interest in music than their Western and Nordic peers. However, even after adjusting to the lower prices, they have a much smaller cultural budget than people in the richer countries.

2.1.3 Purchasing power

• Households have lower purchasing power than in Western and Northern Europe. This reduces record sales. • Households spend a smaller amount of their income on recreation and culture and they tend to spend more on basic needs. This also reduces record sales. • Prices are lower in Central Europe, which has a positive effect on sales. However, this is more the case in live music and synchronization. The prices of the physical product, mechanical royalties have a global price, and the VAT level is generally high in CEE. Often there is no price differential in digital services. Songs can be downloaded from Bandcamp at the same price all over the world. Only some products, such as Spotify premium subscriptions are taking into consideration the lower purchasing power in Central Europe. • The combination of the three forces gives the effective purchasing power on recreation and culture at PPP. CEEMID contains all variables to analyze and project such differences, and we are already making inroads to account for sub-national, regional differences, because while Slovakia or Hungary are less affluent than Austria or the Netherlands, Bratislava and Budapest are among the richest cultural city-level markets in Europe.

The details will be available with some sub-national regional insights the Croatian, Hungarian and Slovak national reports and in custom analysis for CEEMID users.

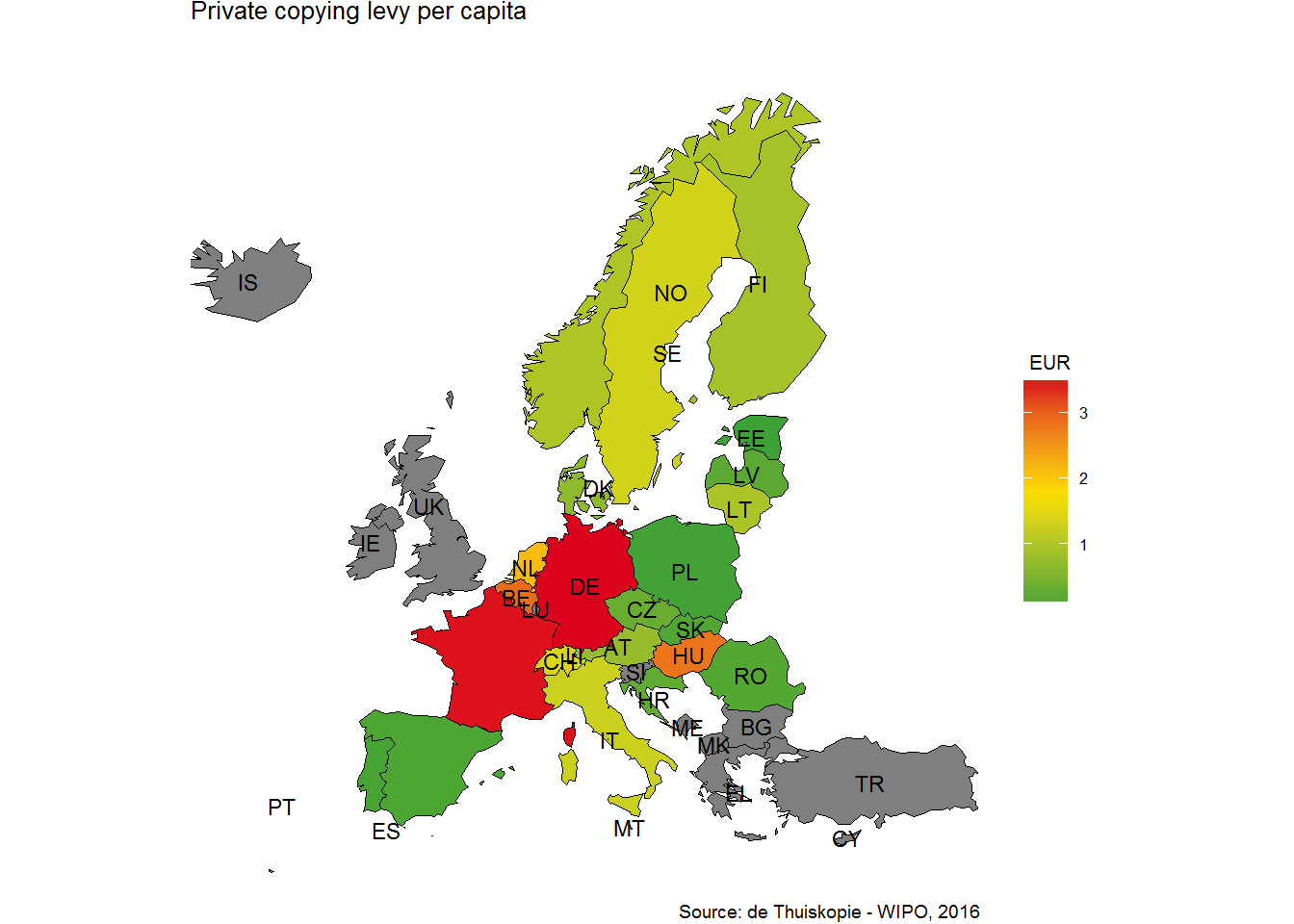

The gap between the similarly great demand and the pricey supply is filled by home copying and illegal torrenting, which plays a bigger role in Central Europe than in Western and Northern Europe. Home copying is exempted from royalty payments all over Europe, but record owners are entitled for a compensation in the form of private copying remuneration (PCR). There is no single European private copying regime, and different member states offer different level of protection to the home copying content. The availability and level of PCR is critical in the Central European markets.

The descriptive statistics about PCR collection, distribution and legal models is available from the de Thuiskopie-WIPO surveys.

Ten years ago there was a general optimistic view on the market that the 60-years-old European PCR regime will be obsolete in the new area of digital music distribution. However, home copying and torrenting is still a major force even on the more developed markets, and it is extremely important in emerging markets where often legal digital services are not available. In fact, the United Kingdom has just recently introduced a PCR system and Slovakia has brought its old and dysfunctional system in par with Hungary and Austria.

CEEMID is often used as a source to calculate fair compensation for private copying. We conduct nationally representative surveys in several countries to establish the actual volume and market value of the music and audiovisual works copied in these countries. Such input data is used by our pricing model that can set appropriate tariffs for broadcasting, public performance tariffs, the price level of licensed digital services or the fair compensation of private copying.

2.2 Investments in the Recording Industry

The music industry relies on creativity and novelty. Generally new individual releases, unheard songs and recordings are more valuable than pieces in the evergreen backcatalog, even if the already much larger backcatalog potentially creates higher revenues. New recordings are the main media for music discovery. Especially young people who listen to more music than older generations want new songs. Investments into the recorded repertoire is critically important for individual artists and bands, but currently labels do not finance these investments, because the profitability of the sector is very low. Due to digital technology, recording costs have fallen in the past decades, but after the rise of internet and widespread piracy the value of recordings have fallen, too. The recording industry traditionally relies on micro-enterprises, namely independent recording studios that offer recording facility for artists. Traditionally recording costs had been reimbursed by labels based on an exclusive recording agreement, but in smaller markets, especially in smaller emerging markets there are very few record labels who can finance new recordings and can pay artists significant advance payments. Currently Central European labels mainly focus on the promotion and distribution of already existing recordings. Most of the recordings, often even in the case of music published by recording labels is financed by the performing artists. Even though IFPI regularly publishes Investing into music reports, such reports do not have emerging-market specific data. In our view, CEEMID offers the only reliable information on the CEE market, because labels and their producing associations do not possess and process much information on this subject. Our data is based on music professional surveys which are filled out by artists, managers, producers and technicians.

2.2.1 Recording artists

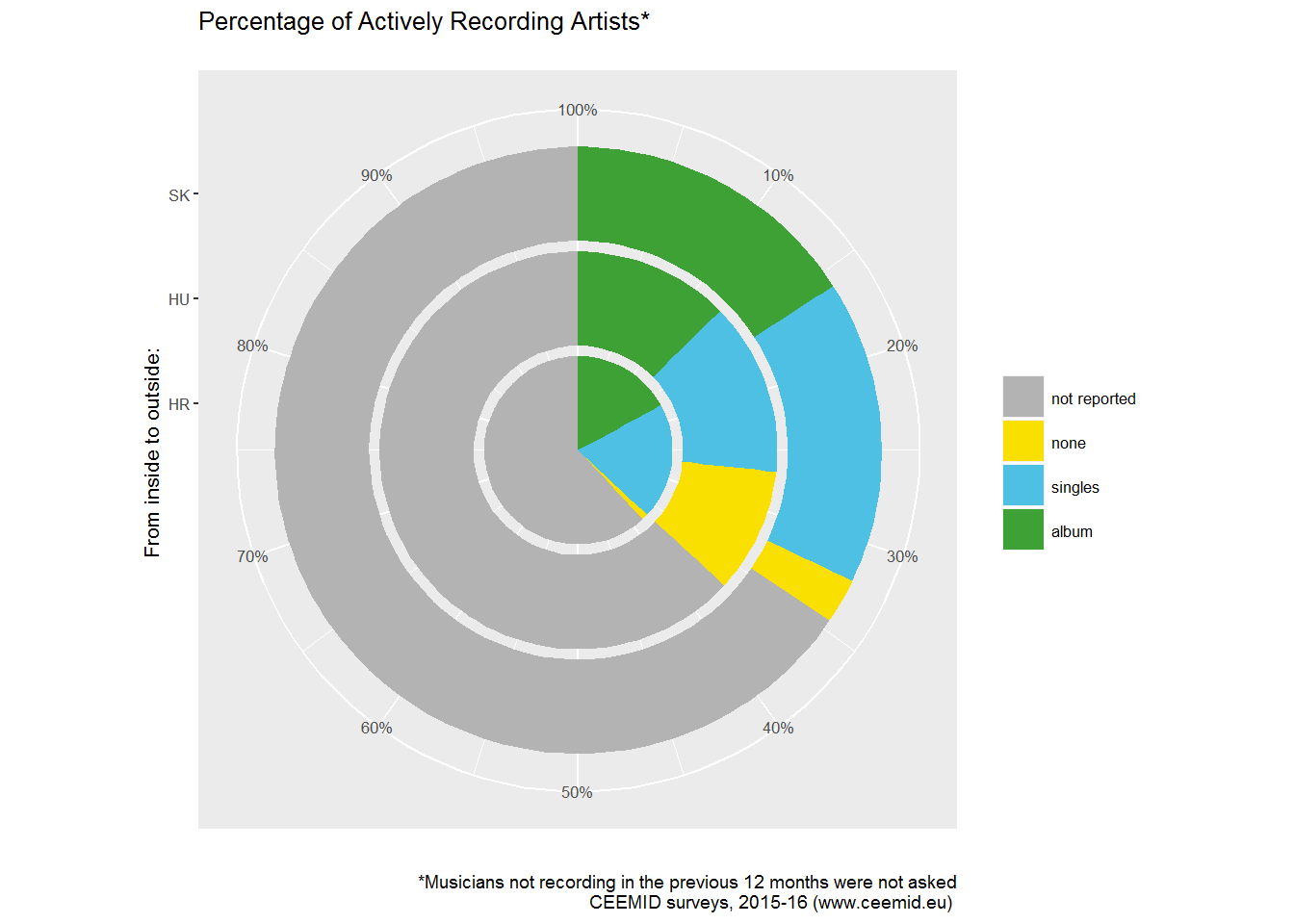

Each year about a third of the active musicians creates new sound recordings. We are collecting data on label-published, self-published, demo, film, software game and other production recordings. In all three surveyed countries, significantly more recordings are self-published than distributed via a label.

Musicians and their managers often underestimate the complexity of music promotion and distribution. While labels hardly finance recordings any more, but they have a very important role in physical and digital distribution, stream marketing, and promotion in radio and background music channels. In Central Europe public performance yields more revenues than digital and physical sales combined, but distribution in these channels is extremely difficult for self-published artists. No wonder that even though only a minority of the recordings are published by labels, almost all the performance revenue is collected by these producers.

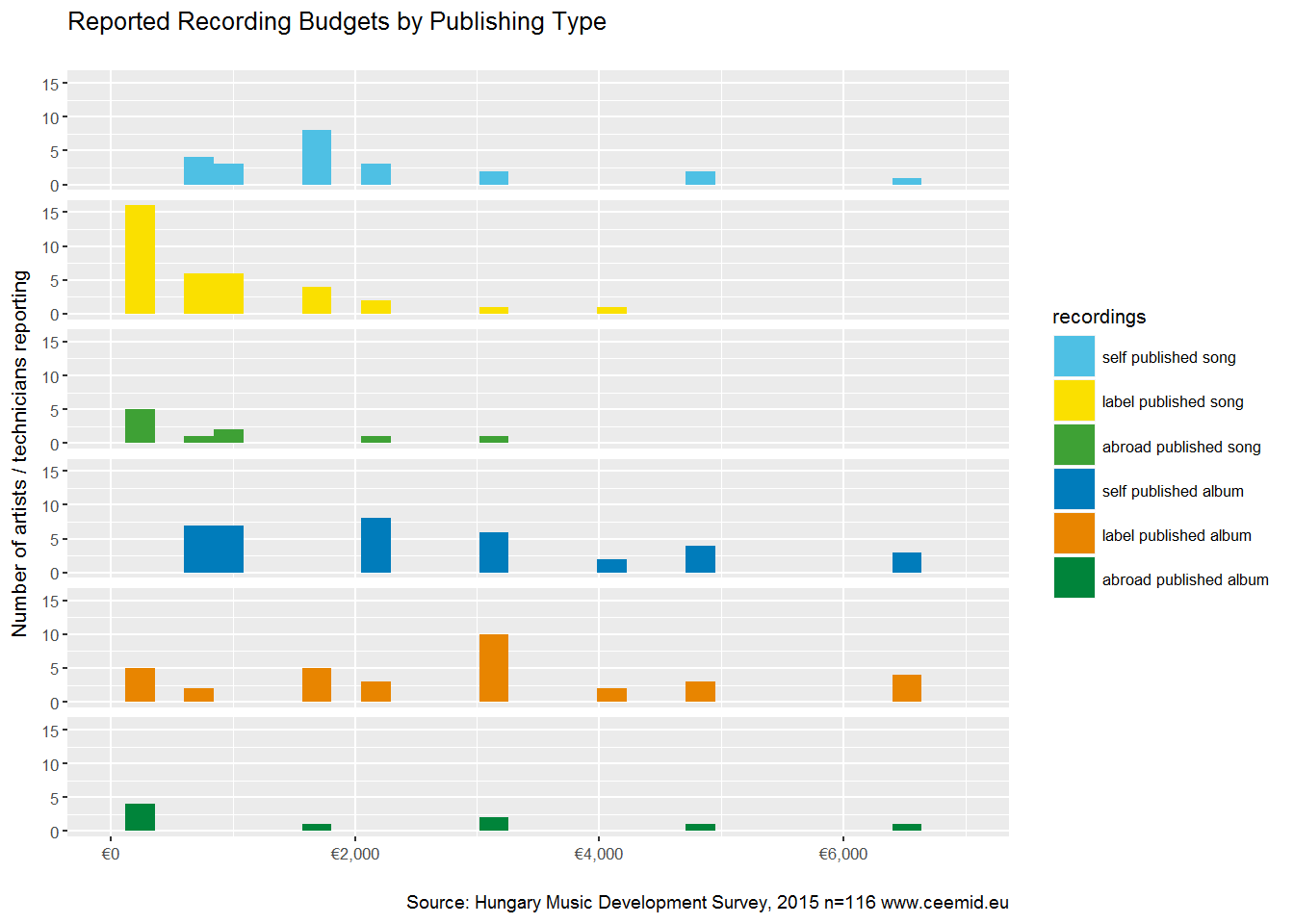

2.2.2 Recording budgets

Recording budgets were only asked in the Hungary Music Development 2015 survey. There are follow-up surveys planned in Slovakia and potentially in Czech Republic, too.

(#fig:recording_budgets)Recording budgets in the region