Chapter 4 Live music stream

The live music income stream is currently the most important for the artists, and also for the policy-maker, because it has the largest employment and value added effect for the national economy, and especially in Central Europe it also creates large tax income for the treasury.

Currently the live performances yield the most revenue for the popular, entertaining music and it is also the most important revenue source for the musicians worldwide, and this is the case in Central Europe, too. In the United States and the United Kingdom the live performances surpassed the earlier dominant recording industry around 2008-2009 as the main revenue source. (Michaels 2009).

It is not very easy to provide national or regional statistics on live music, because concert promotion is a very decentralized activity. As opposed to the recording industry and authoring activities, the value created in live music is not well represented in UN or EU standard statistics. In the national statistics, most elements are reported under NACE 90.01 - Performing arts, 90.02 - Support activities to performing arts, 90.03 - Artistic creation, and 90.04 - Operation of arts facilities. These categories include theatrical and other performing activities.

There is a continuum of performing arts from non-musical theatre to music, including opera, operetta and musical. The technical and management support staff that creates theatrical productions, including stage and lightning professionals, physical workers in transport or security functions are all shared among performing arts. Thus the employment of live music performance cannot be statistically separated from other performing arts without special purpose data collection and surveying.

Furthermore, all over the EU, concert promotion, booking and performing is mainly made by micro-enterprises and artist-entrepreneurs who are subject to simplified financial and statistical reporting in all EU countries. Our surveys were designed to address these shortcomings. Some of our findings can be made only in the larger context for cultural and creative industries, and addressed in the scope of a wider economic and cultural policy agenda.

4.1 Live music audience

Our live music market demand estimates are based on the survey results of 21900 interviews concducted in the region, which are nationally representative for each country. We have estimates for total market revenue, total concert audience, likely concert audience by demographics and sub-national geography.

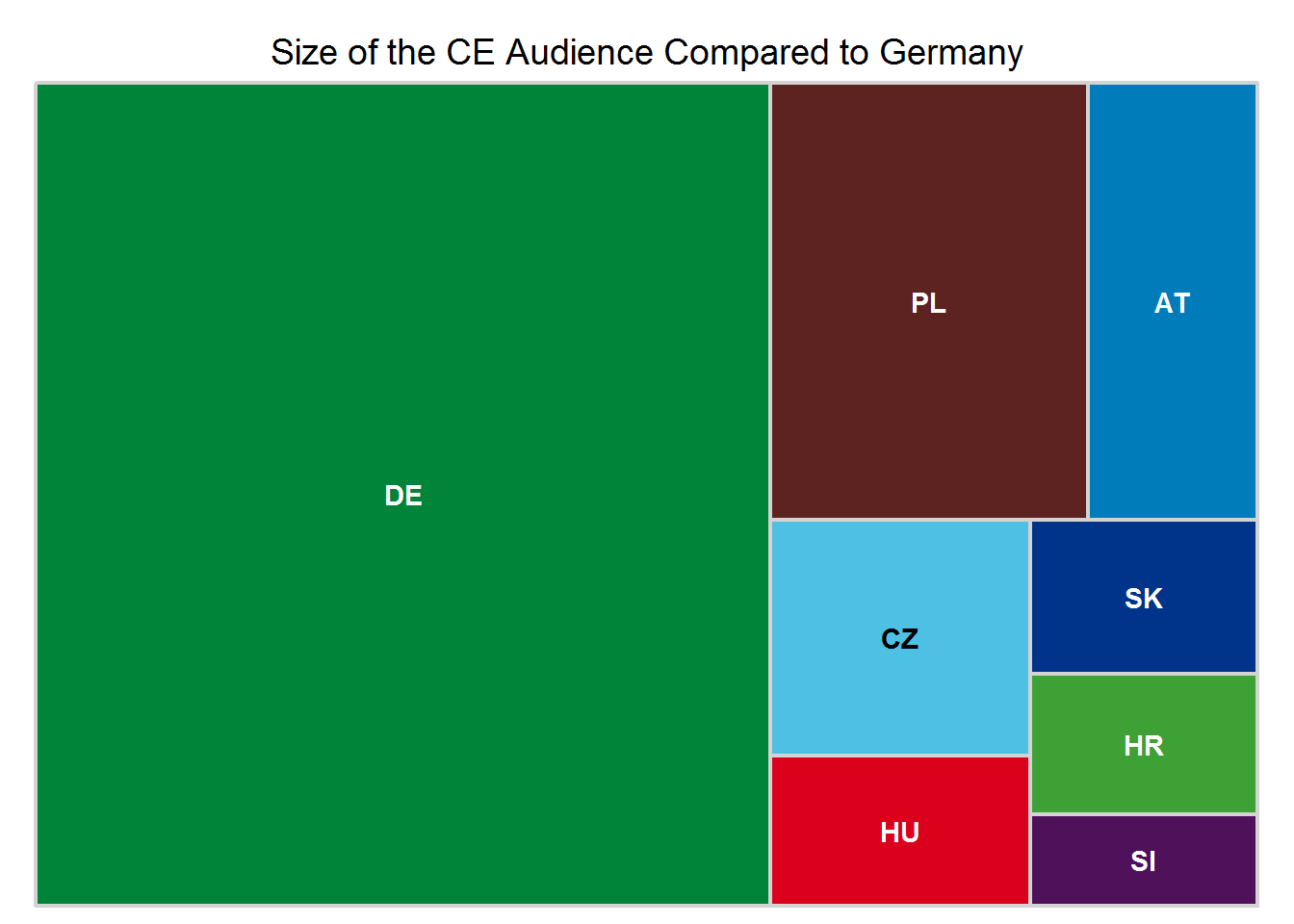

The size of the Central European concert market in turns of visitors and concert visits is somewhat smaller than the German market. The largest domestic market is the Polish market, which is much less affluent and has less foreign visitors than then the Austrian market, and is likely to be significantly smaller than the Austrian in euro turnover.

The third market is the Czech market. The adult population of Austria, the Czech Republic and Hungary is roughly the same, and this is also the order in purchasing power and visiting probability. It is worth noting that while the Austrian market exhibited significant growth in the last decade, the Czech market significantly worsened between 2007 and 2013, and generally the Czech visiting statistics are no better than the Slovak values.

(#fig:age_audience_size)Size of the CE audience compared to Germany

Hungary and Slovakia have similar sized domestic markets, even though Hungary has a much bigger adult population. This is due to the fact of the higher purchasing power and higher concert visiting probability of the Slovak households. However, Hungary’s Sziget Festival adds far more foreign visitor than Slovakia’s Pohoda. Budapest has many venues, including the A38 Ship and MÜPA that sell many tickets to cultural tourists throughout the year. In fact, Budapest due to its bigger size, even after adjusted for the lower purchasing power is a similar sized market than Vienna. Bratislava is a much smaller capital city.

The smaller markets are Slovenia and Croatia. Slovenia has the highest purchasing power and the highest visiting probability in all the new member states of the EU. The size of her market is almost the size of Croatia’s, which in turn has rather demography. Croatia attracts the most tourists in this country group, and a growing number of seaside festivals adds many tickets sold to foreign tourists. ###Audience demography and outlook

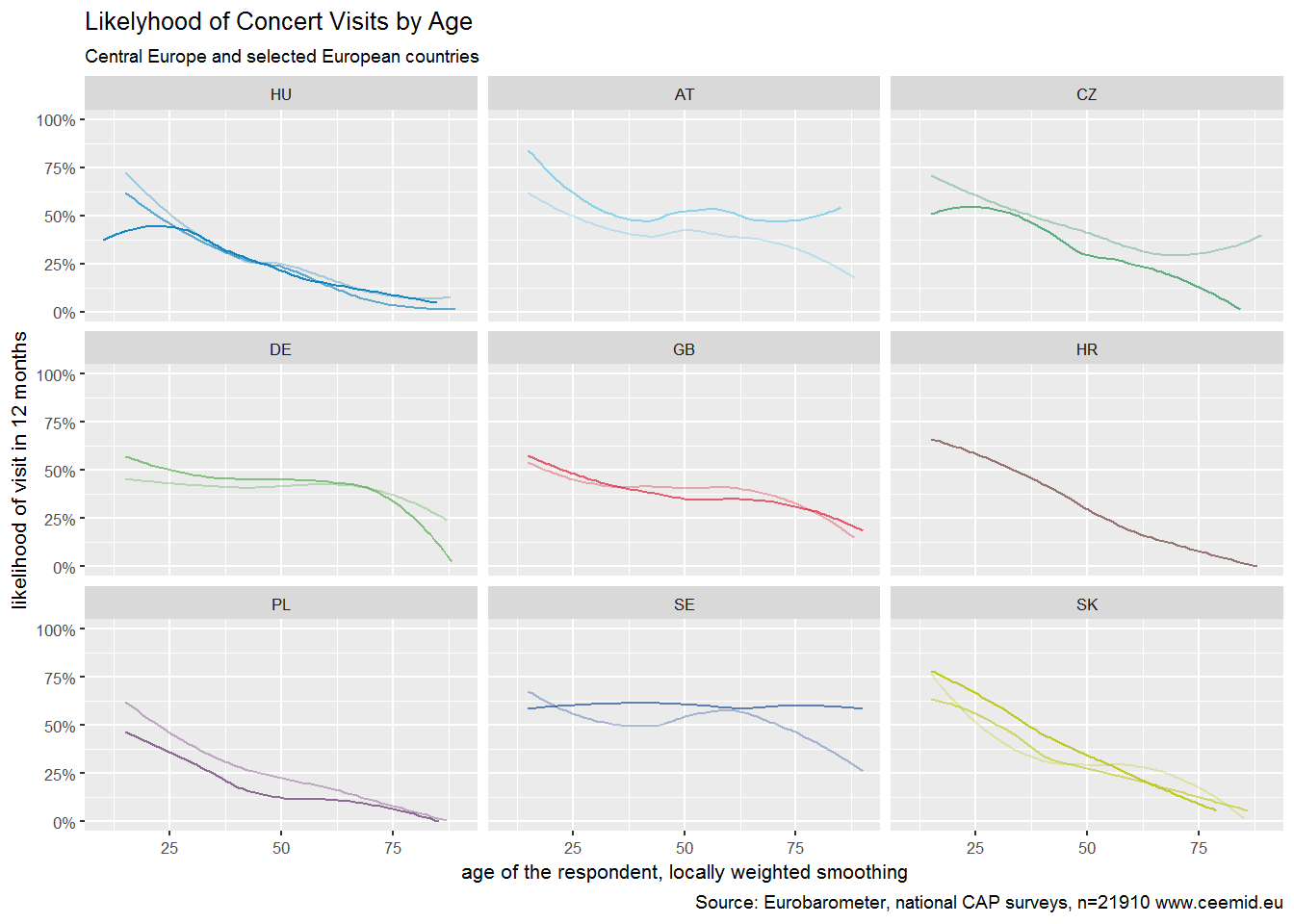

The CEE audience is characteristically different from the Western- and Northern European audiences, and also from the Austrian concert visiting population. In the CEE the audience tends to be significantly younger, on average by 10 years. This is mainly since in the CEE concert visiting is declining by age. This poses a very significant challenge for middle-aged musicians, because their fans are staying at home. It is also a problem for the concert promoter because the highest earning segment of the population is not showing up in the clubs. In the past years that situation worsened significantly in Poland, the Czech Republic and Hungary, and stayed the same in Slovakia. These countries experienced a severe economic crisis in the last decade and an exodus of young people towards the West and the East who were the primary audience of the local shows.

However, especially for young and upcoming artists the CEE is a particularly interesting tour destination. Prague has an excellent touring position, while Bratislava and Budapest are very close to Vienna. These three cities are among the richest European cities with a very young audience. For acts that attract mainly a young audience, Budapest and Prague are no worse markets than Vienna. Bratislava, Ljubljana and Zagreb are touring destinations comparable to affluent Western non-capital cities.

(#fig:age_audience_)Likely hood of concert visits for age groups

The outlook for the region is not very good. As opposed to Austria, or Sweden, where older people who have more free time and have a large enough disposable income concert visits appear to be growing, in all CEE countries it is declining very fast by age. There are several external factors at play, such as low pension income substitution levels after retirement, massive older age unemployment, and poorer health in older cohorts. However, this appears to be a cultural phenomenon as well, because people in these countries already stop visiting concerts in their early middle age. In concert visits this translates into an even larger deficit, because these countries have much worse mortality rates and generally people live shorter lives.

Some of these issues cannot be addressed by cultural policy. However, the lack of middle-aged audience is not a demographically given factor. It is particularly important for the domestic musicians for two reasons. First, because middle aged people can have a much higher disposable income and can afford higher ticket prices, or more ticket purchases. Second, because people tend to identify with performers of their age. The disappearing middle-aged audience forces middle-aged musicians out of business in a decade when live performances provide at least two thirds of the artist income. Attracting the middle aged domestic audience back to the arenas, halls and clubs is a very important business development and cultural policy challenge.

It is worth noting that some genres, especially classical music has an opposite problem. In Hungary, data shows that while the popular music audience is getting younger, the concert hall audience is getting older, because it does not have sufficient supply among younger generations.

Our national reports contain more specific sub-national breakdown and insights into tour management in these countries.

4.1.1 Sub-national differences

The strongest local market is Budapest, which is the most populous city in Central Europe. Hungarian artists report higher average and maximum visitors in the capital city than Slovak and Croatian colleagues.

Croatia is far less centralized than Hungary. Croatian musicians report a much stonger countryside audience than Hungarians. This breakup was not asked in Slovakia.

4.2 Production of live performances

There is no reliable information on the exact number of live performances and the exact revenues of live performances in the region. Neither of the countries have a centralized ticketing system, and in the CE region most tickets are anyway sold at the gate, apart from large arena shows.

The most comprehensive source of information about live performances is the database of the national author’s society. This data source are:

Author’s societies are mainly focusing on information which has a copyright relevance, i.e. concerts where the author is the performer, or did not die earlier than 1947. Rules vary if non-contemporary classical music, jazz and folk music is reported to them or not, and if such information is processed, because there are no author revenues connected to such concerts.

Many concert organizers, especially small venues, try to avoid paying author royalties, and do not report concerts. It is very difficult to estimate the number of unreported shows. Such events usually do not have ticket pre-sales and significant visibility through marketing, and their market value may be very small.

Many performances involve recorded music. In the case of foreground music, when an artist such as DJ is creating a performance, may or may not be reported to the author’s or neighbouring right societies. In case where there is no artist involved, or there is no ticketing in the venue, we talk technically or practically about background music that is covered by blanket licensing. Such events are not recorded but they are also not part of the live music industry, and there are no direct musician earning’s apart from public performance royalties involved.

The ticket revenues are greatly concentrated in the large, arena- and festival events where ticket prices are high and the audience is big. An arena concert may have more revenues than a music club throughout the whole year. For this reason, or national estimates on market euro value are relatively precise, however, they are not exact regarding number of events.

4.2.1 Music clubs and small venues

Most of the venues in the region fall under the category of “small venues”, i.e. venues with a capacity below 1500. The number of venues is decreasing which causes difficulties for artists who rely on concert revenues more than ever in a generation.

The number of venues can be estimated from the licensing data of the author’s societies, and does not necessarily include venues that play non-licensed old classical and folk music. None of the CEE countries have an exhaustive list of licensed venues, which makes tour organization and general business planning difficult. Our research into the development needs of Hungarian artists and technicians revealed a strong need for such a database, which could also include basic technical information about each venue. Such information is well available in Austria.

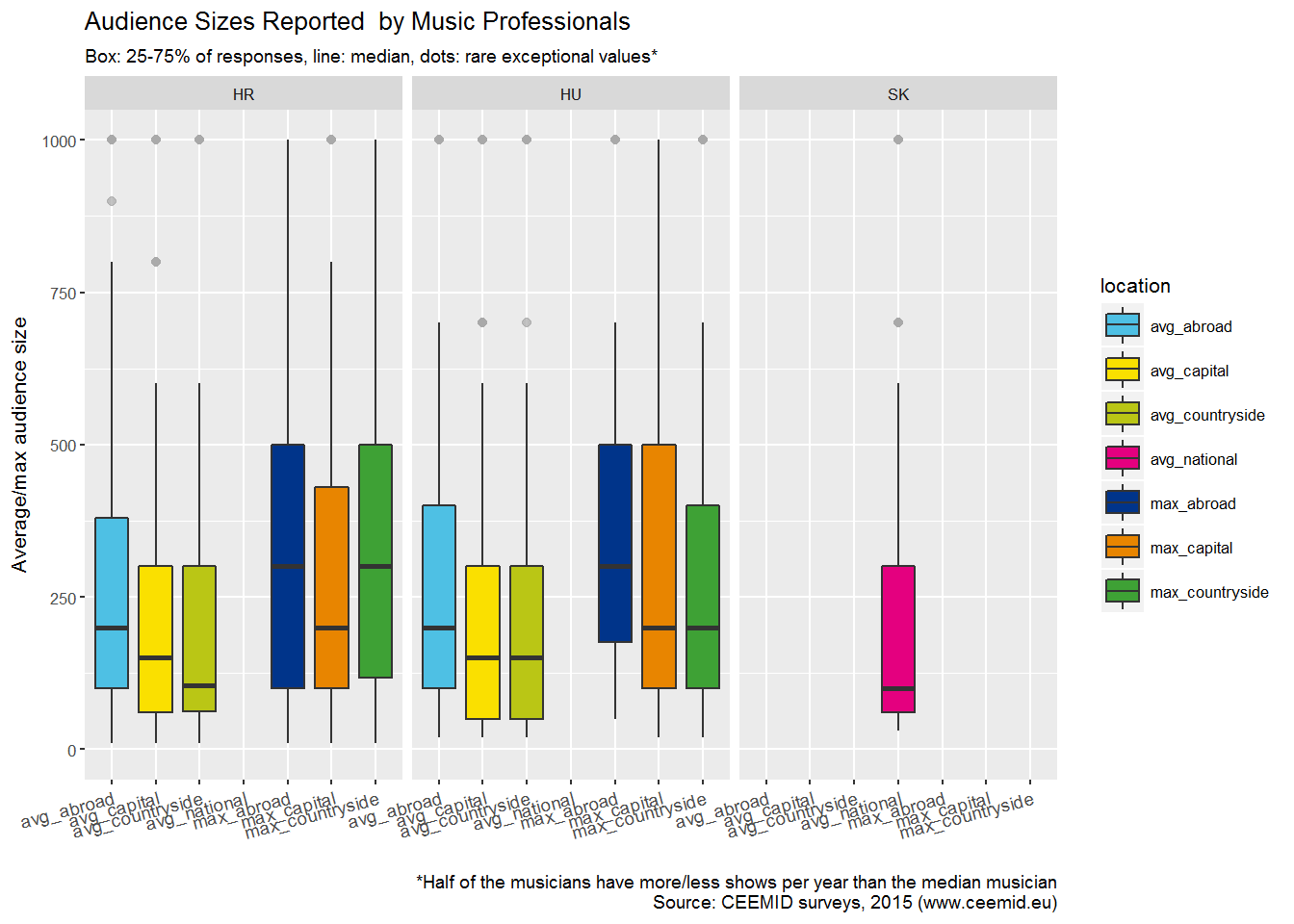

About 75% of all concerts have 50-300 visitors in Croatia, Hungary and Slovakia. The clear majority of musicians never play in front of more than 500 people. The audiences are even smaller outside Budapest and Zagreb. Most foreign shows take place within the region. For Slovak artists, the main target is the Czech Republic, for Croats the former Yugoslavia, and for Hungarians Romania and Slovakia. The audience size tends to be a bit larger in regional tours, given that more successful acts make break out from their subnational regions, but these concerts are take place also on small venues.

Figure 4.1: Audience Sizes Reported by Music Professionals

Live music requires a costly infrastructure with significant fixed cost, and very significant labour input. Given that labour is getting more and more expensive all over Europe, the sustainability of small venues is declining. In Hungary we have witnessed an annual loss of venues at the rate of 25% per year.

Many small venues have obsolete technology and infrastructure that makes touring more expensive and the overall audience experience less attractive. The layout of older venues often do not comply with safety regulations. Because local equipment is obsolete or non-existent, touring acts need to transport rented equipment. The layout of the older venues makes transportation and installation of non-permanent stages and technology difficult and expensive.

This is a similar problem experienced by small movie theatres which needed to invest into digital projection in the last decade. In more affluent countries, smaller towns often built 21st century multi-purpose cultural centres with modern stage and projection technology. While such cultural investment requires a large upfront investment, the use of modern digital technology makes the variable costs of staged and cinema events much smaller. Such modern venues are very rare in the CEE.

For small venues, the licensing of music is often a relatively large administrative and financial burden, too. In our view, the problem of the small venues requires more attention from all stakeholders. Collective management societies are usually not involved in this problem, because the revenues collected from the small venues are very small in the total income. However, the small venues are extremely important for the career prospects of their members: they are the gates to build a lasting relationship with the fans and the venues of the most important live income stream.

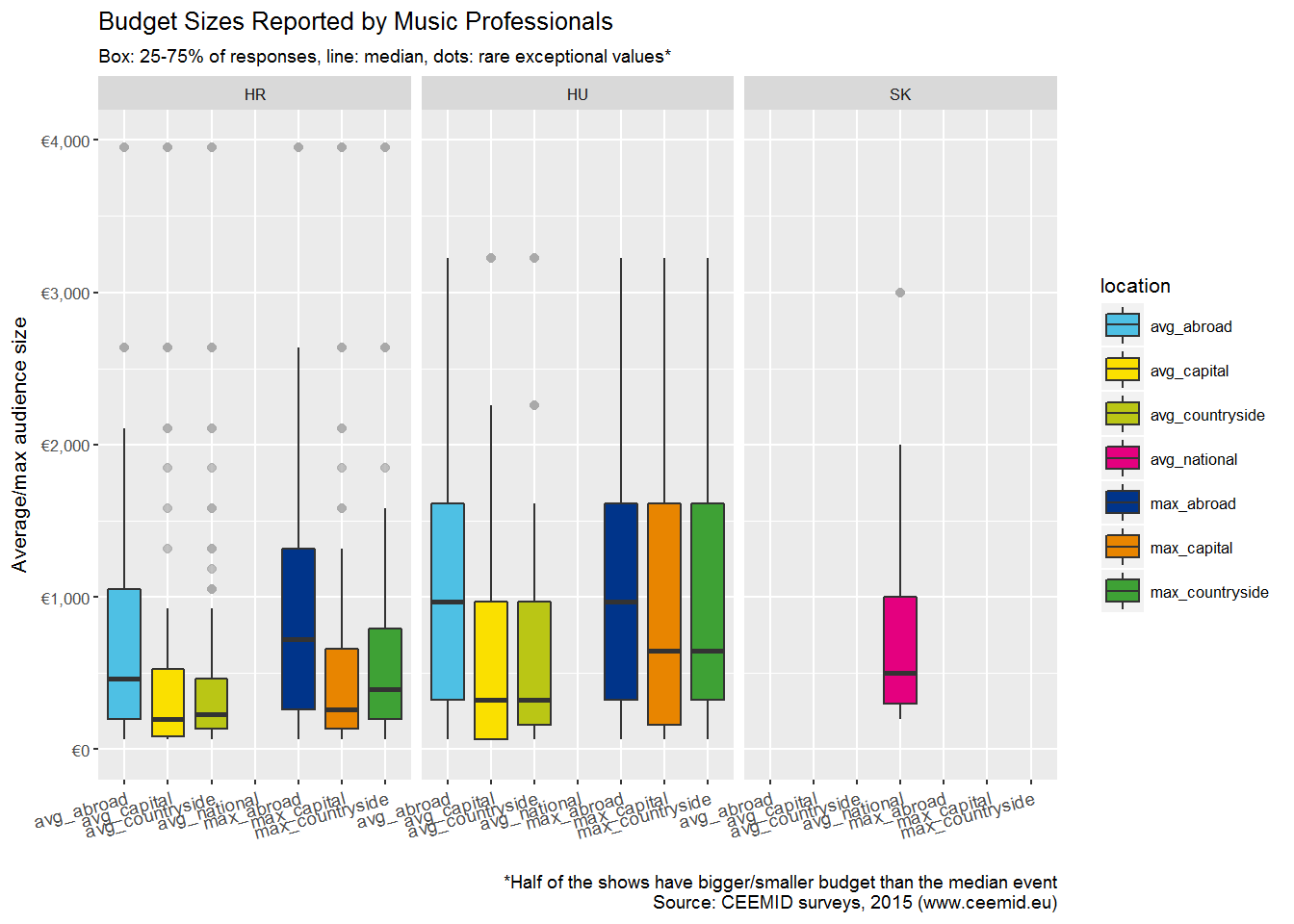

Figure 4.2: Budget Sizes Reported by Music Professionals

Most of the shows have a budget below € 1000. This amount is shared by typically 4-5 musicians and 4-5 supporting staff, including technicians and transporters, and authors via the live music licensing fee.

4.2.2 Arenas

Larger venues are very scarce in the region. In Budapest, the Budapest Arena operates at full capacity and promoters believe that its monopoly position is not beneficial for the market. Bratislava has no similar sized venue. Due to the large infrastructure cost, modern arenas are like modern small venues: they can accommodate various cultural and sports events.

Arenas event budgets are running well in the multiple € 100,000 budgets, and provide entertainment for tens of thousands of people. They account for a very large part of the total market.

Vienna has a very strong position in the concert market due to her proximity to Bratislava and its better infrastructure. Many shows are viable only in Vienna. The Budapest Arena also attracts a high number of visitors from the Slovak Republic and even Belgrade in the absence of similar stages for global acts.

4.2.3 Festivals

The CEE region is the currently the centre of the European, and arguably, the world music festival scene. Apart from Tomorrowland in Belgium, only CE festival had so far won the European Festival Awards in the major festival category. (Sziget, HU – 2011, 2014, Open’er, PL – 2009, 2010; Exit, RS – 2013 ; Untold – RO, 2015)

Festivals can partly substitute for a stable local demand and a quality infrastructure. With combining the audience of many performances, they can reduce the risk of individual acts and appeal for a more affluent Western audience. Concentrating shows and audience to a few days, they can provide a high-quality infrastructure that is not available during the season in most CEE towns.

The CEE regions’ festivals are very competitive compared to Western festivals, because they require plenty of labour and access to good locations that is cheaper in the region. Sziget, for example, employs about 9000 people. At this level the access to lower wages is very important.

The major festivals of the region are very appealing for a foreign audience. This is especially the case for Sziget, where most the visitors is non-Hungarian, or in the smaller festivals on the Mediterranean cost of Croatia and Montenegro. Such festivals are a mixed-blessing for the domestic industry. Due to their appeal for cultural tourist they tend to stage international acts, so the local musicians do not profit from this sudden increase of demand. In fact, local promoters often complain that the expensive, international festivals often drain the budgets of young people. On the other hand, the work opportunity for non-artist music professionals, especially stage, lightning and sound technicians is crucial to stay in business. While they are not only serving domestic musicians on these festivals, the earnings in the festival season keeps them in business and makes their services available throughout the year.

The significance of festival is far greater than in Germany or other developed markets. In Hungary, festivals account for almost half of the total market.

4.3 Concert economy

The CEEMID Music Professionals Datasets contains survey results from 2996 music professional in Croatia, Hungary and Slovakia. Most of the respondents are active musicians, but several hundred surveys were filled by technicians, such as sound, light or stage technicians, managers, producers, educators and music journalists. It is a comprehensive data source on the working and living conditions of music professionals.

The database consists of 432 variables, metavariables, and hundreds of textual comment fields. The large number of variables are due to the fact that some questions are specific to about 80 professionals roles in the industry, such as teaching music or recording music. These variables can be grouped and compared.

Based on this data we can calculate how many live performances and recordings are need to sustain a full-time musician career. We also track hybrid-careers, where people take other part-time technical, managerial or unskilled roles in the broader music and performances industry to support their part-time music career.

4.3.1 Number of performances required for full-time musician career

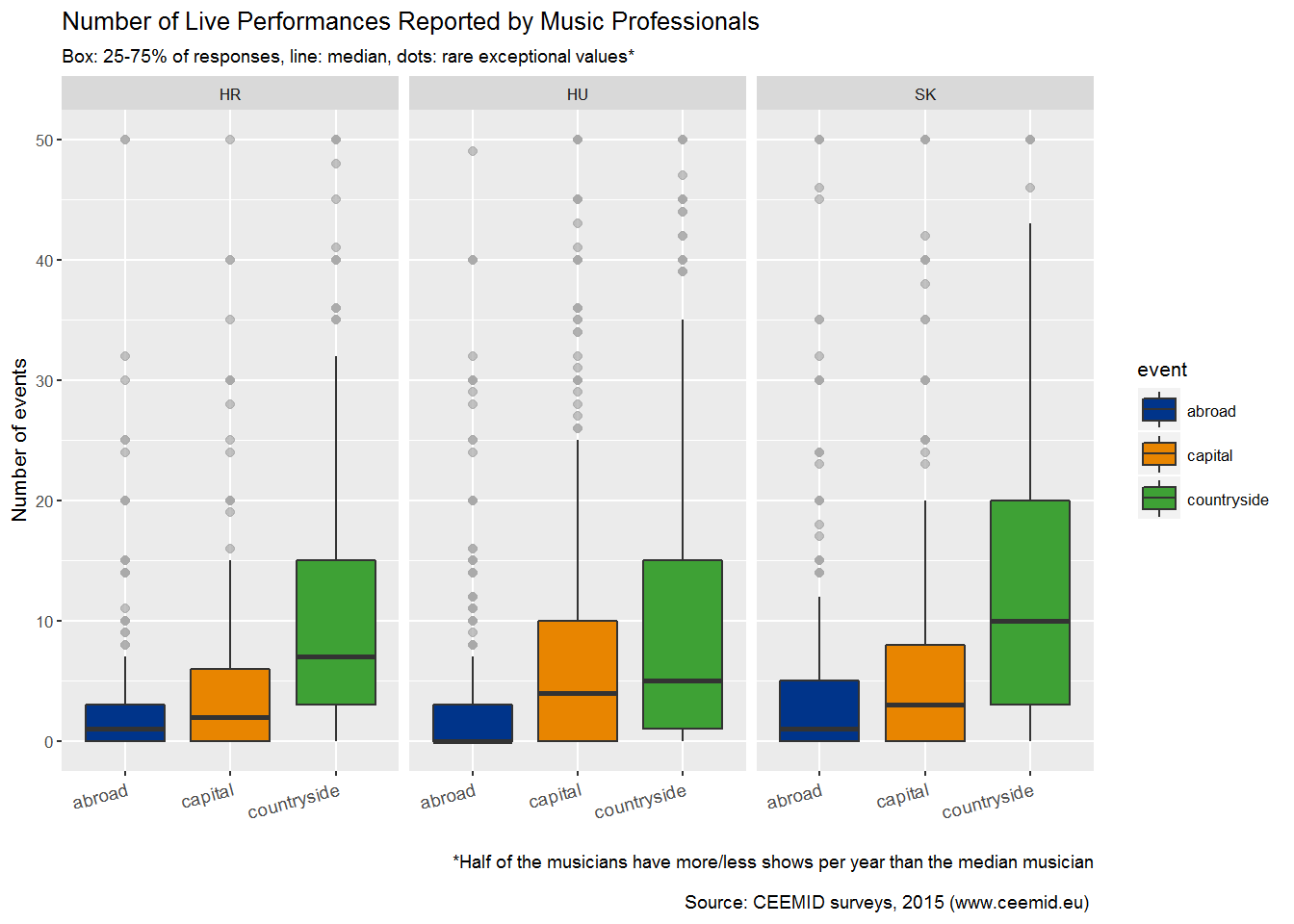

It appears that the Slovak musicians have the most live performances, and the Hungarians the least. Slovaks often play in the Czech Republic and Croatians in the former Yugoslavia. Hungarians tend to have less opportunities both abroad and in the countryside.

(#fig:event_number)Number of Live Performances Reported by Music Professionals

4.3.2 Electronic music

A comparision of performing DJs and musicians.