Chapter 1 The Music Industry

1.1 Music among creative and cultural industries

In the past two decades there was a growing interest for market activities related to culture and creative content. One of the reasons of this global trend is the reduced financial and organizations participation in certain cultural domains by the state. The other important aspect is the high but atypical employment capacity of the cultural and creative industries (CCIs). Because the traditional economic statistical nomenclature of the 20 century is more focused on industrial production and homogenous industries, it turned out that CCIs have a hidden employment, investment and tax potential that had been overseen by economic policymakers.

In the past 8 years considerable effort was put into achieving a common framework on a global (UN) and on European (EU) level. These methodological and conceptual works had been concluded and published by Unesco (UNESCO Institute for Statistics 2012) and Eurostat (Bína, Vladimir et al. 2012). Currently the EU and the UNESCO uses a highly harmonized approach which treat the music industry similarly. The EU Digital Agenda and the Green Book on Cultural and Creative Industries refined this and harmonized approach in the past years, and the European grants in the Creative Europe framework also follow these concepts.

1.2 The three income stream model for the music industry

The three income streams model is essentially a value chain based model that was developed in the United States (Hull et al. 2011) and adopted by the European Commission’s Joint Research Center for European CCI policy purposes. (Leurdijk and Ottilie 2012). We made minor adaptations in the three income model for applicability in Central Europe. The light blue insert in Fig.1 highlight other, music-related CCI links, such as manufacturing and sale of music instruments, etc.

While in the original American model sound recordings are the “main” income stream, currently, especially in Central Europe the live performance stream earns the most income for a typical musician. The author’s stream is the oldest, traditionally and analytically first part of the music industry that includes revenue streams based on musical works exploited by music publishers and via author’s CMO societies such as SOZA. In the US it is called the publishing stream, but in Central Europe it is dominated by authors’ societies, so we modified the label.

The music industry became divided in 1909 when the U.S. Supreme Court denied copyright protection for phonographic rolls. The phonographic industry which changed from rolls to record plates and later to CDs and digital albums sought intellectual property protection in the form of neighbouring rights. The exploitation of neighbouring rights creates separate revenue streams for record publishes and self-published musicians. From the 1930s the recording industry far surpassed the music publishing business worldwide and became the dominant revenue source for the whole industry till the 2000s.

In the 2010s the live performance stream creates the most revenues in many developed and emerging markets, and it is especially important in Central Europe. The live performance stream has an exceptionally strong input to employment, given that live performances create jobs in transportation, in the venues and the connecting accommodation, food and beverages industries, where many enterprises cannot serve their clients without live or recorded music. Food and beverage services are itself second largest European employer after construction and its tourism-related segment is also a large service exporter. Unlike the other two streams, live performances do not receive but pay musical royalties to the authors. Neighbouring rights are not involved unless the live performances are recorded and published in audio or audiovisual recordings.

1.2.1 The changing musician career

In the 21st century there was a very significant change in the music industry that greatly affected the professional lives of musicians and the wider profession, including technicians and managers. The recording industry lost its flagship role in creating revenues and financing performer careers. First with the rise of internet piracy and file sharing, and later with the ubiquitous presence of far larger repertoire on music streaming services than ever made the actual revenues of new songs and albums far smaller. Even though digital technology made recordings much cheaper, the music industry is still again driven by live performances. In the early 21st century, just like the early 20th century, most musician’s career is driven by live performances. The audience can copy all the recordings, can stream all the songs every made, but that makes the magic of the live performance just even more attractive.

Our survey of about 3000 musicians reflect this change. Musicians who started their careers in the analogue age usually started recording after 5 years stage presence. They often played the songs of more established songwriters first, and started to make compositions in the hope of royalties even later. The new musician in the digital age first creates her music in the home studio, than creates a recording, and after digitally releasing the songs starts to seek for a live audience. There are far more recordings made these days than 20 or 40 years ago. However, there are far less stages to play all over Europe. We will analyze these changes in depth in the subsequent chapters.

The CEEMID Music Professionals Datasets contain survey results from 2996 music professional in Croatia, Hungary and Slovakia. Most of the respondents are activemusicians, but several hundred surveys were filled by technicians, such as sound, light or stage technicians, managers, producers, educators and music journalists. It is a comprehensive data source on the working and living conditions of music professionals. The database consists of 432 variables, metavariables, and hundreds of textual comment fields. The large number of variables are due to the fact that some questions are specific to about 80 professionals roles in the industry, such as teaching music or recording music. These variables can be grouped and compared.

What does this mean for the modern musician? Apparently, career advice and routines from the earlier decades are not valid in the 2010s. In the analogue age, musicians used to compete with a limited repertoire available in the radios and record shops, and they slowly gathered their fan base on the tour. Currently, the musicians are facing a competition of 40 million or more tracks on various digital channels, and they need to find a way to an audience who is willing to pay for the more valuable live performance. Building up a fan base on YouTube and Spotify requires a very fresh mindset.

Cultural policymakers, such as music funds, cultural funds, music exchange centers and public broadcasters also need to modify their strategy to promote the national music repertoire. They have to learn that the most important channels, such as YouTube and Spotify are very difficult to address on a national level.

1.3 Central European market characteristics

1.3.1 Purchasing power

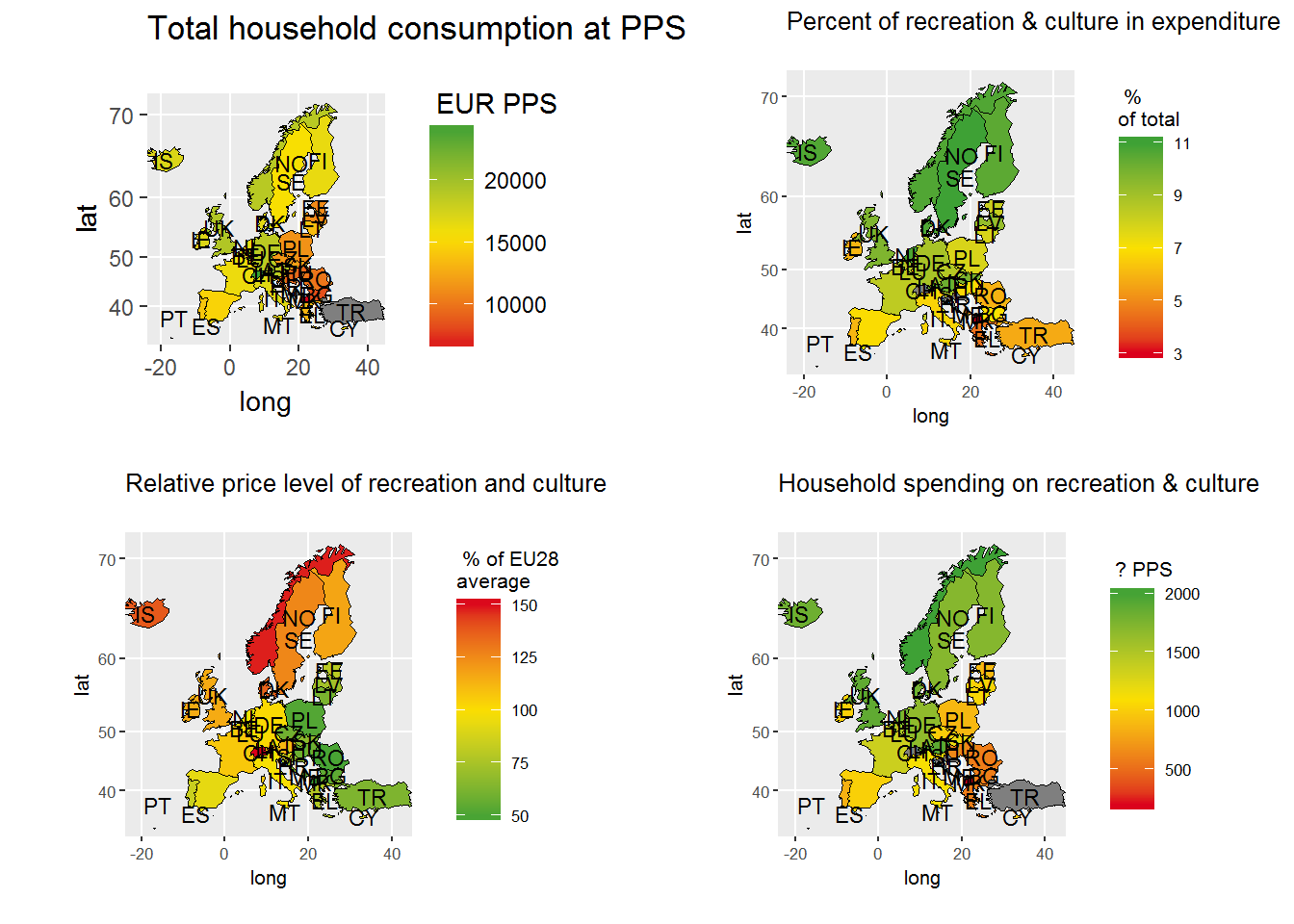

Households have lower purchasing power than in Western and Northern Europe. This reduces record sales.

Households spend a smaller amount of their income on recreation and culture and they tend to spend more on basic needs. This also reduces record sales.

Prices are lower in Central Europe, which has a positive effect on sales. However, this is more the case in live music and synchronization. The prices of the physical product, mechanical royalties have a global price, and the VAT level is generally high in CEE. Often there is no price differential in digital services. Songs can be downloaded from Bandcamp at the same price all over the world. Only some products, such as Spotify premium subscriptions are taking into consideration the lower purchasing power in Central Europe.

The combination of the three forces gives the effective purchasing power on recreation and culture at PPP. CEEMID contains all variables to analyze and project such differences, and we are already making inroads to account for sub-national, regional differences, because while Slovakia or Hungary are less affluent than Austria or the Netherlands, Bratislava and Budapest are among the richest cultural city-level markets in Europe.

The details will be available with some sub-national regional insights the Croatian, Hungarian and Slovak national reports and in custom analysis for CEEMID users.